Inflation hasn’t been that much of a concern for companies in recent years – or rather excessive cost increases haven’t. In fact, the lack of inflation has, at times, been troubling to businesses, making them query their investment decisions and worry about the prospect of diminishing potential returns their investments result in. It has also raised concerns about debt levels, which might remain higher over time relative to flat earnings returns.

Yet as the global economy starts to recover from the pandemic, alarm bells have begun to ring among a number of NatWest Markets clients about the prospect of higher inflation.

We believe a return of inflation could lead to a number of potential problems for businesses:

- Labour cost & supply issues: Labour shortages, which are now affecting many industrial, construction and services firms, have prompted some wage inflation. The same businesses have expressed concerns that supply shortages and wage inflation could endure.

- Commodity prices: as measured by the Commodity Research Bureau (CRB) index, the prices of raw materials have doubled since hitting lows during the pandemic, and are now 7% higher than at the end of 2019.

- Freight costs: shipping costs have risen sharply due to container shortages and rising transport costs. The Baltic Exchange Dry Index, a measure of dry bulk shipping costs, shot up by almost 240% between the end of December 2020 and early May.

- Additional pandemic-related costs: more debt, coronavirus-linked social distancing measures, minimum wage hikes, the end of rent and rates holidays, and the prospect of higher taxes to finance generous government support are all going to mean higher costs for companies.

- Supply chain disruption: supply chain disruption resulting from the pandemic and Brexit has become more widespread, as have rising input costs – although we’re also seeing a certain amount of speculative price increases being fed in. Meanwhile, the potential need for multi-jurisdictional supply chains to overcome trade frictions related to Brexit and the pandemic could lead to further supply chain pressures.

- Retail demand & demand-pull inflation: the UK headline retail sales volume index from the ONS rose to 113.6 in April 2021. But it’s unclear whether this is just a result of pent-up savings and demand combined with easing lockdown restrictions and price discounting, or a sign of more persistent changes in behaviour and spending patterns – which could result in demand-pull inflation.

What do these risks mean for companies?

Shortages of skilled labour represent a significant risk factor. In manufacturing, construction, health & social care and parts of hospitality, the latest lockdown has resulted in labour shortages. The firms we’ve talked with believe this could prove a medium- to longer-term problem rather than a near-term issue. While unemployment hasn’t risen as much as some had feared, the fall in labour force participation, albeit only 1%, could reflect a more permanent change in the domestic labour supply.

The years that followed the global financial crisis (GFC) may be particularly informative on the risk posed by rising commodity prices. The global economy has become quite used to cost push-inflation (when overall prices rise due to higher input costs) since the global financial crisis of 2008-09, when there was a significant bout. After sinking to multi-year lows in 2009, the CRB index, a measure of the prices of a broad basket of commodities, rose by over 75% in the space of less than 2.5 years. That rise in commodity prices was in part speculative rather than due to shortages. The recent signs of commodity price inflation we’ve seen – notably the doubling in commodity prices since March 2020, according to the CRB index – are therefore not unexpected. But this time the increase may in part be driven by supply-side issues rather than purely due to demand-side, ‘speculative’ activity.

Freight costs are on the up, making supply chains more expensive. The Baltic Exchange Dry Index rose from just over 1350 at the end of December 2020 to a peak of 3266 in early May. That’s because over the past 6–9 months there’s been a growing shortage of shipping containers in Asia to ship goods to the West. With limited transport of goods from Europe to Asia, the UK and Europe have accumulated a glut of containers – making shipping from the Far East more difficult and expensive. The short-term solution has been to include the cost of shipping the empty containers back to their port of origin in the cost of shipping goods. This could become a longer-term solution unless more goods are shipped from the UK and Europe back to Asia.

Additional pandemic-related costs need to be dealt with. Firms that have been forced to close for extended periods during lockdown have taken on extra costs. These include expenses associated with becoming more coronavirus-secure, taking on extra debt to stay afloat, and delaying rent and rates payments. These factors, combined with reduced capacity limits resulting in a drop in income, are likely to lead to increased prices (which we’re already seeing in some areas of services).

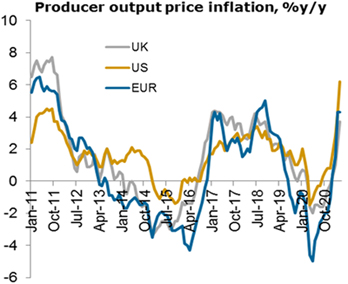

Supply chain disruption is becoming more commonplace in the wake of Brexit and the pandemic. Firms involved in construction, manufacturing and wholesale have repeatedly referred to supply shortages, with demand outstripping supply in a variety of materials and semi-manufactured goods. This is clear in the pace of producer output price inflation, although this has, so far, risen more quickly in the US and the euro area than the UK.

In construction and some areas of manufacturing, materials prices have risen sharply due to shortages and some speculative price hikes (to take advantage of the supply/demand imbalance). The chart below makes it clear how producer price inflation has spiked. But it’s important to remember that it’s not the level of producer price inflation that’s the issue – it’s the speed of the move from deflation to inflation, which has been much faster than anything we’ve seen over the past decade. Nevertheless, the firms in these sectors that face materially higher input costs tell us that their clients seem to be less resistant to the prospect of higher prices than they’d envisaged