10 Jun 2021

Biodiversity TNFD and investments

Biodiversity is increasingly being used within the context of finance, as reduced biodiversity is an increasing problem.

When you think of biodiversity, what do you think of? A David Attenborough documentary? The variety of species we have? Evolution? It’s a broad term that is increasingly being used within the context of finance, as reduced biodiversity is an increasing problem, with voluntary initiatives failing to address the issue.

Increasing evidence has highlighted risks from nature loss over the coming decades. c.50% of global GDP is moderately or highly dependent on nature and its services. This creates material risks and opportunities for financial institutions, asset owners and asset managers, as they lend or invest in companies facing increasing threats associated with biodiversity loss. However, the world’s ecosystems have already diminished by 47% globally, relative to the earliest estimates, with 1 million species at risk of extinction. Therefore, this is not just a financial consideration but survival.

The United Nations (UN) Biodiversity Summit has been delayed due to COVID-19 and is currently expected to take place in October 2021 in China, ahead of COP26. This conference aims to have countries agree to a global biodiversity framework with internationally binding targets for biodiversity (akin to the 2˚C of the Paris Agreement for climate) providing a guiding light for all market participants. It is proposed that milestones by 2030 will be interim stepping stones for 2050 goals, including increasing the area of natural ecosystems by at least 5% globally and halving the number of new introductions of invasive species globally.

Whilst at a supranational level, work is still being done to establish ‘value’ and agree targets for biodiversity, it is arguably a slower process to integrate this into financing efforts. At present, many projects that damage biodiversity are not explicitly punished, nor conservation of biodiversity explicitly rewarded. The emergence of KPI-linked products for a number of asset classes continues to rise, with this being one area that could be considered. Whilst climate measurability is challenging, biodiversity is even more complex given the interconnectivity and far-reaching impact. It is not surprising perhaps that disclosure and reporting around biodiversity has not been as high on the agenda as climate change metrics, such as emissions, but there is growing recognition that this is an area of material importance.

Whilst the Task Force on Climate-related Financial Disclosures (TCFD) is increasingly used by many asset owners, managers and corporates to report climate-related intent and purpose, the newer Working Group for the Task Force on Nature-related Financial Disclosures (TNFD) created last year and formally launched last week, is hoping to be embraced as the equivalent for natural capital. The current thinking includes a 'double materiality' approach i.e. both how nature impacts a company and its operations, in addition to how the operations of a company impact nature. However, more work is needed to distil this into straightforward measures that financial market participants can track, monitor and report.

As Barbara Pompili, France's Minister of the Ecological Transition, said: "The challenge of biodiversity and nature preservation is crucial. We need corporate and financial institutions to take their parts. Yet, we lack unified definitions, standards and metrics to accurately and thoroughly embrace nature preservation. The TNFD will constitute an important step to start properly addressing at [the] global level biodiversity-related risks and impacts."

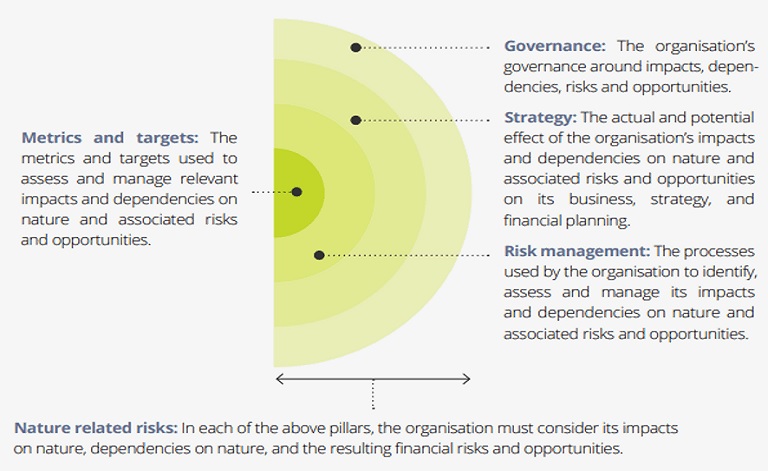

The TNFD, like TCFD, will use a four-pillar approach (governance, strategy, risk management and metrics & targets), shown below. By 2023, they will deliver a framework to report on nature-related risks to shift financial flows towards ‘nature-positive outcomes’ and/or reduce the ‘nature-negative outcomes’.

TNFD four pillar approach

Source: TNFD’s Nature in Scope Report (2021)

TNFD's definition of 'nature-related risks' is distinct, since it goes beyond the short-term financial risks but also incorporates the longer-term risks associated by an organisation’s impact and dependency on nature. Although different from TCFD, there are similarities in approach and financial materiality, which will also incorporate transition risks, as well as scenario analysis or stress testing. Once again, financial institutions, central banks and regulators are deliberating how environmental risks and opportunities should be managed in the future to create nature-positive outcomes.

What has been done before?

With no global consensus on disclosure for nature, the Banque de France, as an example, started analysing the biodiversity impact of its investment portfolios in 2020, which included two impact metrics.

- Biodiversity scores: which reflect commitments, measures and outcomes of the companies invested in (e.g. formal policy/information published, etc.)

- Indicators of exposure to companies involved in the production of substances harmful to biodiversity (e.g. pesticides, etc.)

When asked why Banque de France chose these impact metrics, Gautier said "the short answer is: because they were available … we need collective participation to identify a wider range of indicators. That's why I expect a lot from the TNFD. When you focus on disclosure then you can help companies to participate in this disclosure. I don't expect the TNFD to identify precise data necessarily but at least identify some topics which are useful to report."

There’s been a flurry of recent reports including the recently published ‘A Market Review of Nature-Based Solutions: An Emerging Institutional Asset Class’ which finds that nature-based solutions provide a growing opportunity to invest in activities to protect and restore ecosystems. With current spending of biodiversity conservation currently at $130billion per year, the report argues private investment must be scaled to meet the >$700billion financing gap annually.

In addition, Finance for Biodiversity's ‘The Climate-Nature Nexus: Implications for the Financial Sector’ argues that both climate and biodiversity risks need to be considered together rather than in isolation, which is arguably the more favoured current approach given the interconnectivity.

Like TCFD, TNFD is intended to shape private capital flows; however engaging with financial policy makers and regulators remains a priority, such as the Network of Central Banks for Greening the Financial System (NGFS), the G20, G7, as well as standards bodies such as the International Financial Reporting Standards, TCFD and other relevant initiatives, given the importance of reporting and disclosure requirements, which we have seen in climate. Data will once again play an important role.

Other biodiversity developments

Whilst many businesses have promised to source key supply chain materials responsibly, it is difficult to measure and compare. The University of Cambridge Institute for Sustainability Leadership (CISL) has recently published the Biodiversity Impact Metric, a risk-screening tool for supply chain businesses that source agricultural commodities, in order to indicate a business’ impact on biodiversity.

A new ENCORE (Exploring Natural Capital Opportunities, Risks and Exposure) biodiversity module enables financial market participants to explore their portfolio’s impact on species extinction risk and loss of ecological integrity (particularly for agriculture and mining). It is an extension of their online tool visualising the links between the economy and nature by the Natural Capital Finance Alliance.

Despite challenges with data, momentum is building, and goals are starting to be publicised by institutions. For example, Kering has committed to having a net-positive impact on biodiversity by 2025.

Next steps

With the newly launched TNFD and UN Biodiversity Summit expected later this year, 2021 is already shaping up to be a big year for improving biodiversity awareness and debate. Whether it means adopting the new natural capital framework being developed, or using new tools and methodologies to measure the impact on biodiversity, asset owners and investment managers, as well as financial institutions, need to build on their understanding of biodiversity – both its risks and opportunities – with regard to their portfolios, and how investment and lending choices going forward will factor this component into the decision-making process, particularly relative to other ESG metrics.

Undoubtedly, this will require knowledge sharing and collaboration between stakeholders to accelerate the expertise and best practice to incorporate this analysis into business processes. Governments, regulators and central banks will also play a significant role to create international reporting standards, as well as supporting the data collection and generation. Considering how an organisation impacts and depends on nature, and the resulting financial risks and opportunities is an area we cannot ignore.

Posted in:

Keywords:

Latest insights

How collaboration and innovation can transform AIFs

We surveyed 100 fund influencers and interviewed leaders to explore how tech is reshaping funds and how service providers can support the shift.

03 Nov 2025

Evergreen funds rising popularity

Evergreen funds are experiencing a growth in popularity thanks to their flexibility, liquidity and resilience to market conditions.

24 Mar 2025

Is nature ready to move into the mainstream?

Nature may be a sideline investment strategy for many asset managers but initiatives to protect the natural world are taking root.

16 Jan 2025