13 Mar 2023

What we’ll see in Jeremy Hunt’s Spring Statement

Here’s what our specialists think we’ll see when the Chancellor reveals his Budget on Wednesday – and what that may mean for the economy and markets.

The Autumn Statement was delivered in the context of weak economic growth, high inflation, and rising interest rates. The Spring Statement seems set against an improved backdrop: a less severe economic downturn, larger tax haul, lower-than-expected wholesale gas prices, and warming weather.

This is a welcome boon for government finances. Indeed, with elections less than two years away and the Tories slumping in the polls, there is some pressure on Chancellor Jeremy Hunt to recycle those savings into fresh spending. Put in realpolitik terms, a key question that could go some way towards shaping the Budget is: to what extent will any newly available fiscal headroom be used now, and how much deployed closer to the election?

The chances of sweeping fiscal giveaways seem, to us, remote at best. But we do anticipate some measures to ease the cost-of-living squeeze (an extended energy price guarantee) and think we may see targeted tax reforms and incentives to get businesses investing (reforms to the “super deduction” tax relief).

Here is what we think you should look out for in the Spring Statement, and the key implications for the economy and markets.

Energy price support: extension for households, more targeted help for businesses

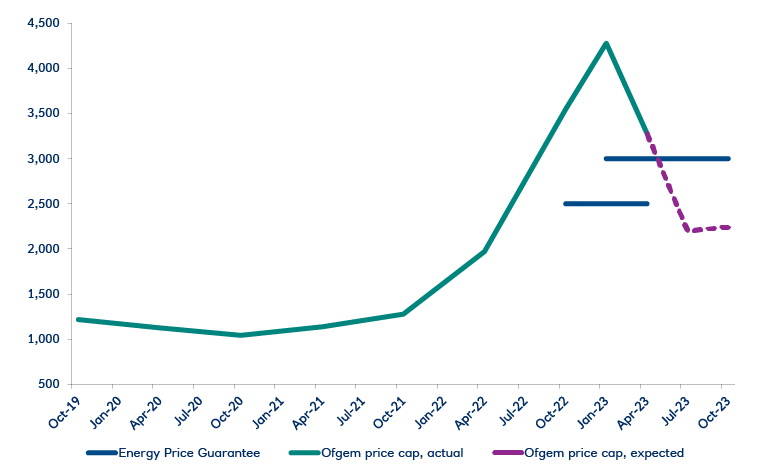

Lower-than-expected spending on energy support measures – notably the Energy Price Guarantee (EPG) for households (capping the typical annual bill at around £2,500) and Energy Bill Relief Scheme for businesses – have been big drivers of government savings over the winter season.

We think the Chancellor will extend the EPG scheme at the £2,500 level by a further three months (it was initially due to rise to £3,000 on April 1) in order to give wholesale gas prices more time to fall – potentially to levels that would make the EPG redundant.

Given the evolution of wholesale gas prices (see chart below), even the £2,500 guarantee would probably only be relevant for one calendar quarter (April-June 2023) as the market-based Ofgem price cap is projected to fall to roughly £2,100 by July.

Domestic energy use: average annual household bill (£)

Sources: HM Treasury, Ofgem, Cornwall Insight, NatWest Markets

Support for businesses will become more targeted under the Energy Bills Discount Scheme (EBDS), which comes into effect on April 1. However, given the trajectory of wholesale prices, it seems unlikely that the Chancellor will offer businesses further help with energy costs.

Fuel duty freeze: positive for fleets

The fuel duty – which hasn’t been raised since 2011 – is supposed to rise by retail price index (RPI) inflation in April, which would add 7p to the price of a litre of fuel.

A temporary 5p fuel duty cut, announced in March 2022, is also due to expire at the end of March. Combined, these would trigger a 23% increase in fuel prices, or roughly 12p per litre.

To avoid this steep increase, the Chancellor is likely to freeze fuel duty for 12 months. Mr Hunt is reportedly also keen to continue the 5p cut, as long inflation is falling. This would keep fuel prices steady at current levels.

Corporations tax: unlikely planned rises will be scrapped, but targeted reforms are a possibility

The Chancellor may, however, offer a longer-term commitment to bringing rates down after a period of growth. He may also introduce targeted tax incentives and measures to boost investment.

One possibility is that Mr Hunt may allow more types of UK-based firms to use investment zones – sites that benefit from tax incentives and less red tape – to lower their blended tax rates and boost regional investment.

He may also look to replace the temporary tax relief on investments – the so-called “super deduction”, which lets businesses to cut their tax bill by 25p for every £1 that they invest in certain kinds of equipment – with a more permanent expensing framework, one that could allow certain equipment investments to be deducted directly from profits.

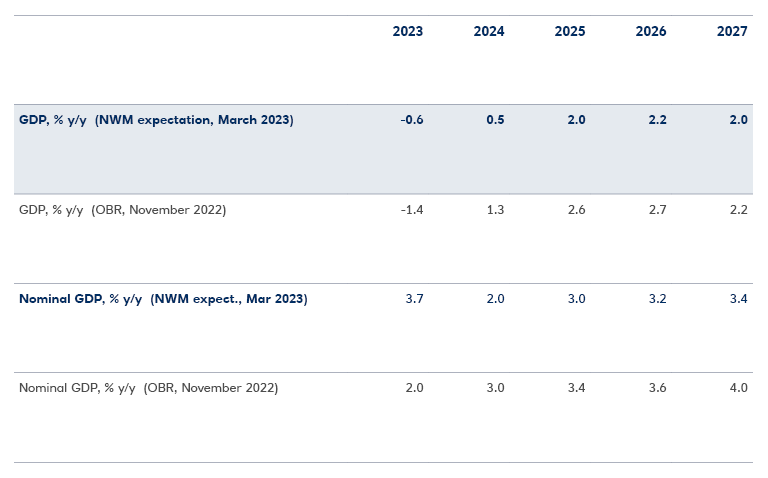

The economic outlook: a shorter, shallower downturn this year, but medium-term headwinds are afoot

As we’ve written recently, the near-term economic outlook has broadly improved: Gross Domestic Product (GDP) performed better than expected in Q4 2022, avoiding a recession; wholesale gas prices have plunged; and business surveys point to greater optimism about the months ahead.

What does all this mean for the economy? The Office for Budget Responsibility’s (OBR) Autumn forecast estimated a 1.4% drop in GDP this year. An upward revision to GDP, to reflect the recent improvement in the outlook, is almost certain.

The medium-term outlook, however, looks less promising. In February, the Bank of England downgraded its medium-term forecasts due to a pessimistic view of the UK economy’s potential to grow without generating inflation. We think the OBR will likely follow suit and trim its medium-term growth forecasts from next year onward.

Medium-term economic growth (GDP %)

Sources: OBR, NatWest Markets

Government finances: the public purse is in better shape, but government borrowing will remain high – putting upward pressure on bond yields

Government finances are looking stronger than anticipated, with a larger tax haul (around 4.5% versus November estimates) and lower spending (around 0.5%) the primary drivers.

This should reduce public sector borrowing in the 2023-24 fiscal year. The Central Government Net Cash Requirement (CGNCR) – the borrowing aggregate which informs gilt issuance – could decline by around £20 billion versus November estimates. Public sector net borrowing (PSNB-ex), the metric that informs fiscal policy, could undershoot its previous vintage by as much as £28 billion.

But with net-gilt issuance (issuance of new gilts minus redemptions) in 2023-24 estimated at around £190 billion– more than triple the annual average in the decade prior – government borrowing remains unambiguously high.

All of this supply comes against a backdrop of very low demand from global investors. For gilts in particular, demand from the major holders (overseas investors and liability-driven investors, or LDI) has not materialised this year, and we don’t expect it to in a meaningful way any time soon.

This supply-demand imbalance should weigh on gilts, with yields on 10-year notes now likely to reach 4.3% by year-end in our view. Rising yields will of course pass through to corporate bond markets, meaning higher borrowing costs for issuers of sterling-denominated securities.

Posted in:

Keywords:

Latest insights

How collaboration and innovation can transform AIFs

We surveyed 100 fund influencers and interviewed leaders to explore how tech is reshaping funds and how service providers can support the shift.

03 Nov 2025

Evergreen funds rising popularity

Evergreen funds are experiencing a growth in popularity thanks to their flexibility, liquidity and resilience to market conditions.

24 Mar 2025

Is nature ready to move into the mainstream?

Nature may be a sideline investment strategy for many asset managers but initiatives to protect the natural world are taking root.

16 Jan 2025