21 Mar 2023

The Spring Budget: the supply-side sharply in focus

Jeremy Hunt delivered a Spring Budget that aims to get people back to work and persuade businesses to invest. Will it work?

Arriving largely as expected, the Spring Budget was positioned by the Chancellor as a “budget for growth” that primarily aims to address two important structural challenges faced by the UK.

The first challenge is weak business investment levels. While slightly above pre-pandemic levels, business investment levels, have stagnated since the Brexit referendum in 2016, which has weighed on economic growth and competitiveness.

The second challenge is weak labour supply in the aftermath of the Covid19 pandemic. Working-age inactivity has increased by around half a million people since the pandemic struck, and employers are struggling to close 1 million vacancies. This has all sorts of implications on the economy, not least driving up wage inflation and making it difficult for businesses to expand.

The growth bump: recession averted, better near-term economic prospects

The economic data has been almost universally positive since the Autumn Statement.

Back in November the Office for Budget Responsibility (OBR) thought the UK economy would round off 2022 in recession, forecasting a 0.4% fall in Gross Domestic Product (GDP) in Q4. Instead, output was flat and the good news has continued into the start of 2023. Business surveys turned upwards in February, with confidence amongst firms in the business services and finance sectors reaching their highest levels since last spring. The labour market is holding up, even with signs of cooling.

With that backdrop it was unsurprising to see the OBR upgrade its outlook for growth in the near-term. Back in November it was pencilling in a 1.4% drop in GDP this year with a potential recession not ending until Q4. That’s been adjusted to a very modest 0.2% drop in 2023, close to the latest consensus view of - 0.5%.

Getting businesses spending again

Most of the policies that appeared in the Budget were well-telegraphed ahead of Jeremy Hunt’s statement in parliament this week.

Notably, the Chancellor also revealed several measures to help businesses offset their tax bill through investments.

The “super deduction”, which lets businesses cut their tax bill by 25p for every £1 that they invest in certain kinds of equipment, is to be replaced by a full expensing programme (initially for 3 years) that will allow the full value of certain equipment investments to be deducted directly from profits. The programme is expected to cost between £8 billion and £11 billion per year.

And he also announced the launch of 12 new “investment zones”. Spread across the UK, these will offer funding and tax incentives to drive growth in key sectors including green industries, digital technologies, life sciences, creative industries, and advanced manufacturing. The government says each zone will have access to tax incentives worth up to £80 million over five years.

Back to work

A number of policies were aimed at persuading more people into work, with a focus on more experienced workers, parents of young children and people with disabilities.

To encourage higher paid 50+-year-olds to stay in work, an increase in the annual cap on tax-free contributions to pensions from £40k to £60k was unveiled. The lifetime allowance above which people incur tax charges was also scrapped. And a new programme of apprenticeships aimed at 50+-year-olds (“Returnerships”) was also announced.

Free 30 hours childcare for working parents with three and four-year-olds has been expanded to cover all children over the age of nine months. However, this will be introduced in stages up to September 2025. Parents on Universal Credit will be able to start claiming childcare costs up front, rather than in arrears. The cap of those claims has also increased by almost 50%. To help with availability of childcare places, each staff member in England will be able to look after up to five two-year-olds instead of four. And the hourly rate paid to childcare providers for free hours will also increase.

These measures, in combination with targeted immigration reforms to attract more builders, are expected to add some 140,000 more people in employment over the next five years, compared with the OBR’s November estimates.

What do these reforms mean for the economic and market outlook?

The government’s supply-side reforms are undoubtedly well-directed, but what do they mean for the economic and market outlook?

Economic growth: a big bump in 2024 with modest downward revisions thereafter

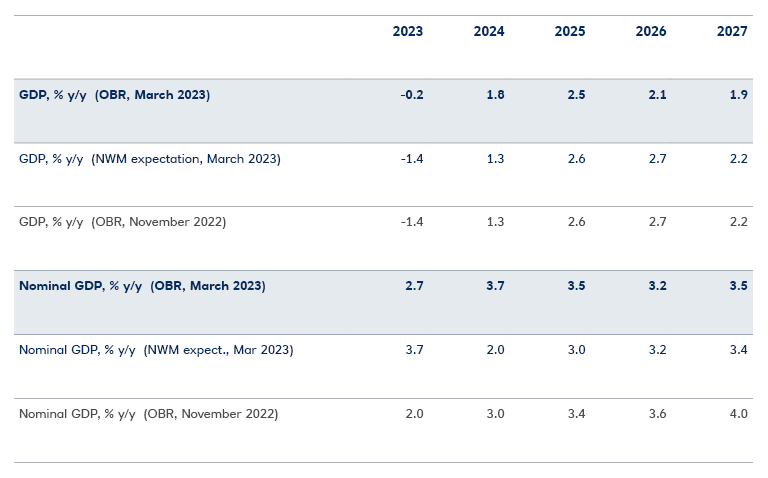

Beyond the near-term revision flagged earlier, the OBR now sees an additional 0.5% growth in economic output for 2024. And from 2025, the OBR’s GDP projections are little altered compared to the November 2022 Autumn (see below).

Economic growth (% GDP) in the UK: a punchy 2024, with modest revisions thereafter

Source: OBR, NatWest Markets

The extent to which capital allowances boost business investment and the impact of measures to spur labour supply are inevitably uncertain, but the OBR’s forecasts appear to take a charitable view compared with others: the Bloomberg survey median sees -0.6% GDP growth in 2023, 0.9% in 2024, and 1.5% in 2025; the Bank of England calls for 0.5% in 2023, - 0.25% in 2024 and 0.25% 2025).

The OBR also remains fairly upbeat on the prospects for an improvement in productivity. Back in November it was forecasting growth in economic output per head of 1.9% through to ’27. That’s had a trim to a pace of 1.6% but it’s still ahead of the 1.3% pace that prevailed in the decade leading up to Covid.

It remains to be seen just how effective the government’s supply-side policies are (or how quickly they impact the real economy). But they are certainly well-guided measures nonetheless.

Public finances: deficits will likely start to drop, but political realities could slow their decline

The OBR’s estimates show that the public purse should continue returning to health despite the government adding some 0.8% in GDP in additional spending each year for the following three – not an insubstantial amount. A rising tax haul and declining government borrowing is forecast to results in the structural budget deficit being eliminated by the 2026-27 fiscal year.

There is a “but”. No government can really bind its successor. With an election expected in 2024, there are no guarantees around the deficit projection. What we can say with greater confidence is that ongoing sizeable structural deficits are likely to materialise over the next two years, with some further discretionary government spending more likely than not ahead of an election later in 2024.

Government borrowing is (still) high, and the direction of bond yields is up

About £241 billion in gross gilt issuance has been pencilled in for the next fiscal year, more or less in line with market consensus – and our own estimate of £232 billion.

But as we’ve flagged in our preview, the combination of historically high funding needs and very low demand from global investors – combined with fresh concerns over financial market stability that weigh more heavily outside the UK – reinforces our view that we’re likely to see upward pressure on gilt yields.

The yield on 10-year notes now looks likely to reach 4.3% by year-end, in our view. Rising yields will of course pass through to corporate bond markets, meaning higher borrowing costs for issuers of sterling-denominated securities.

Posted in:

Keywords:

Latest insights

How collaboration and innovation can transform AIFs

We surveyed 100 fund influencers and interviewed leaders to explore how tech is reshaping funds and how service providers can support the shift.

03 Nov 2025

Evergreen funds rising popularity

Evergreen funds are experiencing a growth in popularity thanks to their flexibility, liquidity and resilience to market conditions.

24 Mar 2025

Is nature ready to move into the mainstream?

Nature may be a sideline investment strategy for many asset managers but initiatives to protect the natural world are taking root.

16 Jan 2025