10 Mar 2023

Monthly UK Economic Outlook: March

Our economists share their views on the key economic trends to watch in the month ahead.

The UK economy only narrowly avoided recession last year, and the outlook for 2023 has improved thanks to a sharp drop in wholesale energy prices, a robust labour market and better global growth prospects. But a word of caution: higher debt servicing costs, the sharp fall in real income and tighter fiscal policy over the remainder of the year are still key risks to watch.

Despite inflation falling, households are still being squeezed, and house prices are succumbing to the sharp rise in mortgage rates. Overall, the going will probably get tougher before the economy gets going.

In a hurry? Watch our NatWest Economist Stuti Saksena share her quick take on the key themes shaping the UK economic outlook in this 3-minute video.

UK economy escaped recession in 2022, but headwinds to persist in early 2023

The UK economy was flat in Q4, avoiding a technical recession. But that doesn’t mean the worst is behind us. The economy contracted by 0.5% in December due to the effects of industrial action, while consumer-facing services suffered as people cut back on discretionary spending. The UK is the only G7 economy yet to return to pre-pandemic levels.

There were some areas of resilience: industrial output rose in December and business investment was up 5% in Q4.

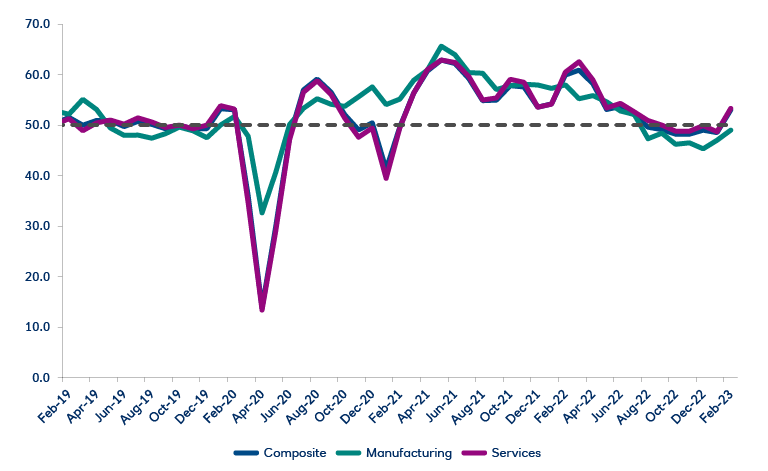

Fast-moving indicators suggest growth has regained some momentum at the start of 2023, with the UK composite Purchasing Managers’ Index (PMI) jumping from 48.5 in January to 53.0 in February. The services sector registered the biggest improvement and there are even chinks of light on the consumer side, with a more upbeat hotels, restaurants, and catering sector. And things are looking less gloomy for manufacturers, with input price pressures abating and supply chains continuing to improve.

Meanwhile, business confidence for the year ahead rose for the fourth straight month, thanks to easing cost pressures and signs of a recovery in business investment.

While all this is encouraging, the PMIs do not cover retail, construction or public services, all of which are under pressure from squeezed consumer incomes, high borrowing costs and industrial action. Household spending remains weak, and household finances continue to come under pressure. Energy grants are coming to an end and bills are still more expensive than two years ago. Higher mortgage interest payments this year will probably deduct another percentage point from annual growth in real disposable incomes. A silver lining may be that despite the cost-of-living squeeze, households have not yet drawn upon their excess savings.

Overall, lower household spending, high borrowing and mortgage costs and likely job cuts mean economic conditions are set to remain weak. Consensus forecasts in February were for a 0.7% contraction of the UK economy in 2023.

UK composite PMI rose sharply in February but a modest Gross Domestic Product (GDP) contraction in Q1 is still likely

Source: S&P Global, CIPS (UK), 6 March 2023

Inflation is retreating but cost of living pressures persist

Consumer Price Index ( CPI) inflation fell for again in January. The headline print was down to 10.1% from 10.5% in December and the 40-year high of 11.1% in October. The biggest cause was core inflation (a measure that strips out more volatile items) easing from 6.3% in December to 5.8%, suggesting that domestic price pressures are finally abating. Services inflation, which the Bank of England watches closely, fell from 6.8% to 6.0%.

What does all this mean for the outlook? Headline inflation looks set to retreat faster than anticipated, thanks to the sharp decline in wholesale gas prices and early signs of cooling wage pressures. Global agricultural commodity prices have also stabilised, supporting a gradual retreat in food prices. Core goods inflation is likely to ease due to lower shipping costs and excess inventories at manufacturing firms, while services inflation is benefitting from lower energy prices.

Despite the improved outlook for inflation, there’s little immediate relief for households: prices are still rising faster than wages. Average real wages fell by 2.5% in the year to December. The latest Office for National Statistics (ONS) survey data shows that 70% of adults report spending less on non-essentials, while a fifth borrowed more money or used more credit.

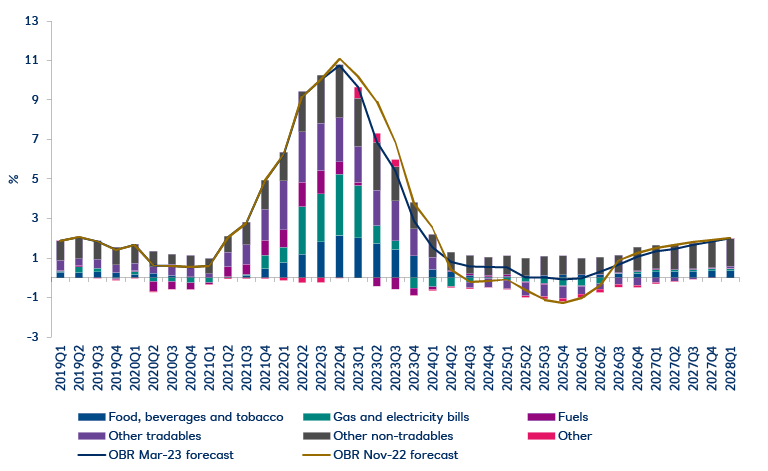

Inflation likely to return to target rate sooner than expected?

Sources: ONS, Bank of England Monetary Policy Reports, Bloomberg Finance L.P, 6 March 2023

UK labour market remains resilient, but slack is slowly developing

December data showed continued strength in employment, while the unemployment rate remained almost unchanged at 3.7%. Redundancies are slowly rising, although they are still historically low at 3.5 per 1,000. Labour demand is cooling slowly, with vacancies continuing to fall from their peak last spring. Survey data also points to a slowdown in hiring in Q1.

Most businesses seem to be adjusting to weaker economic growth and rising borrowing costs by putting hiring plans on freeze. This is likely to lead to the jobless rate rising gently in the coming quarters. Meanwhile, labour supply is on the up, with the workforce expanding year-on-year in Q4.

There are signs of decelerating wage growth. Total pay growth (including bonuses) fell from 6.5% in the three months to November to 5.9% in December. However, wage growth excluding bonuses rose to 6.7% in the three months to December, driven by higher public-sector wages. There might be more to come here given ongoing industrial action and pay settlements.

Overall, the labour market remains an economic bright spot. Most forecasters only expect a modest rise in unemployment to 4.5% by the end of this year.

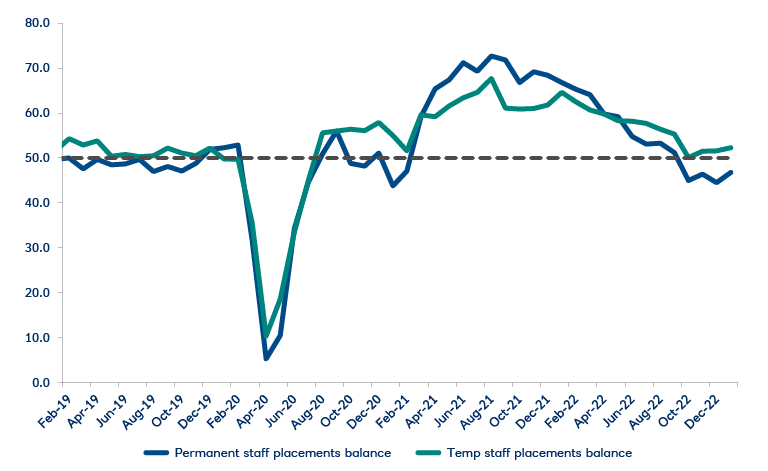

Surveys suggest hiring momentum is waning and permanent staff hiring will deteriorate further

Source: S&P Global, KPMG, REC, 6 March 2023

The tightening cycle is nearing an end

The Bank of England hiked the Bank Rate to 4% in February and indicated it will act again if there is evidence of persistent price pressures.

Our base-case view is that the bank rate will remain unchanged at 4%. That said, further hikes can’t be ruled out just yet. Markets have interpreted strong recent economic data as evidence that more tightening is required (three further 25bp hikes are priced in by September) and the latest PMI reading suggests that growth is holding up better than expected.

While Governor Bailey has attempted to temper some of those expectations, labour market and inflation data in the run-up to the Bank of England’s next meeting on 23 March will be pivotal.

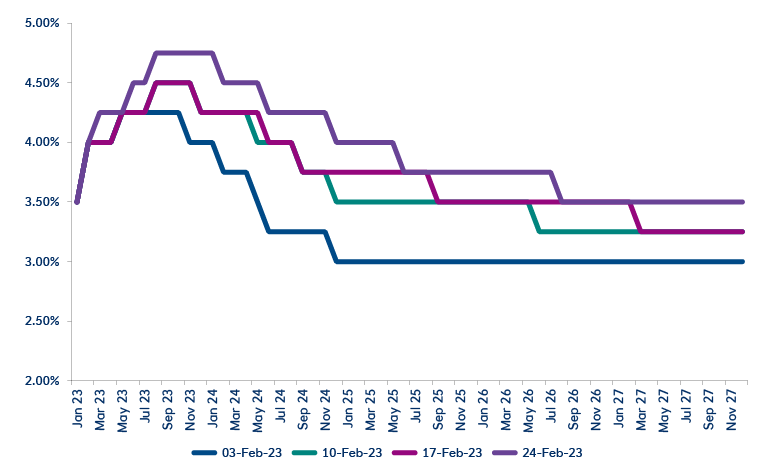

Implied rate expectations inched up to 4.75% in the week to 24 February

Source: Bank of England, NatWest Treasury

Follow us on social media

Be sure to follow us on social media to find out our latest views on the economy the moment they’re published.

Posted in:

Keywords:

Latest insights

How collaboration and innovation can transform AIFs

We surveyed 100 fund influencers and interviewed leaders to explore how tech is reshaping funds and how service providers can support the shift.

03 Nov 2025

Evergreen funds rising popularity

Evergreen funds are experiencing a growth in popularity thanks to their flexibility, liquidity and resilience to market conditions.

24 Mar 2025

Is nature ready to move into the mainstream?

Nature may be a sideline investment strategy for many asset managers but initiatives to protect the natural world are taking root.

16 Jan 2025