14 Feb 2023

Monthly UK Economic Outlook: February

Our economists share their views on the key economic trends to watch in the month ahead.

What a difference a month makes. An air of optimism has emerged at the start of the year, with a sense that 2023 may not be quite as bleak as had been envisioned only recently. The International Monetary Fund (IMF) has raised its forecast for global economic growth, while UK gross domestic product (GDP) was higher than expected in November, boosted by the services sector.

But let’s not get carried away: economists are still pencilling in a mild recession for the UK. If we focus on the positives, inflation has begun to fall from its October peak and the labour market is still an area of strength despite the sluggish economy. Lastly, most central banks, including the Bank of England, are nearing peak rates, and mortgage rates have begun to fall somewhat. Some much-needed relief indeed.

In a hurry? Watch Marcus Wright, Senior Economist share his quick take on the key themes shaping the UK economy in this 3-minute video.

A recession seems to have been delayed rather than averted

The UK economy grew by 0.1% in November – consensus expectations had been for a fall of 0.2%. Support came from both temporary factors (including spending linked to the FIFA World Cup) and various pockets of resilience in the economy (the hospitality and telecoms sectors in particular).

But there were also areas of weakness. Production output fell by 0.2%, dragged down by manufacturing, while construction output was flat. And even if a recession was averted in Q4, the economy looks set to remain subdued over the first half of this year. What’s more, there are few signs that households are ready to splurge those Covid savings – quite the opposite, in fact. Meanwhile, the sharp rise in mortgage rates late last year has resulted in a sharp pullback in housing market activity, with mortgage approvals falling to their lowest level since May 2020.

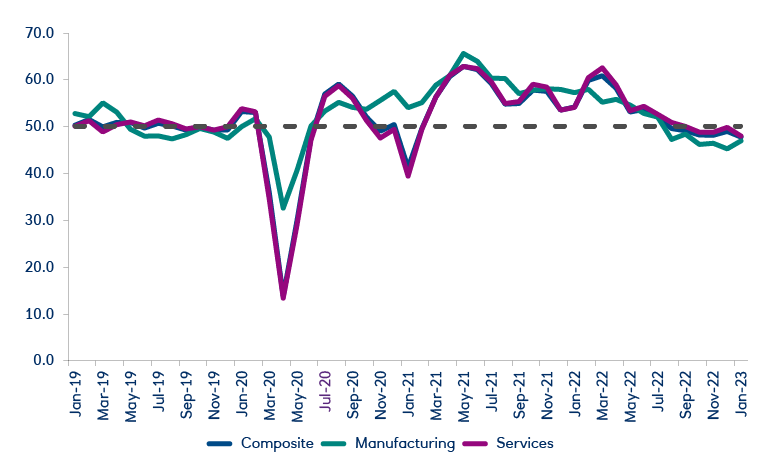

Forward-looking indicators aren’t particularly inspiring. The UK composite Purchasing Managers’ Index (PMI) fell to 47.8 at the start of the year, its lowest level since February 2021, when the economy was in full lockdown. Confidence is particularly low in the services sector. Meanwhile, retail sales fell by 1.0% in December, leaving them 2.5% below 2019 levels. GfK’s Consumer Confidence Barometer fell further in January, suggesting that households may continue to retrench in Q1. Reduced credit availability to households is likely to exacerbate the problems.

There are silver linings. The economic outlook has improved marginally in recent weeks as energy prices have fallen faster than anticipated. This should mean consumer energy bills fall substantially in Q3, boosting real disposable incomes. And businesses are becoming less negative on the UK’s growth outlook for the year ahead, reflected in a much-improved PMI business expectations report in January.

The UK composite PMI fell in January

Sources: S&P Global, CIPS (UK)

Inflation is falling gradually, helped by lower energy and goods prices

CPI inflation fell from 10.7% year-on-year in November to 10.5% in December, mainly due to lower increases in motor fuel prices.

However, food inflation rose from 16.4% year-on-year in November to 16.8% in December, its highest annual figure since 1977. Core inflation, which strips out volatile items, remained unchanged at 6.5% year-on-year.

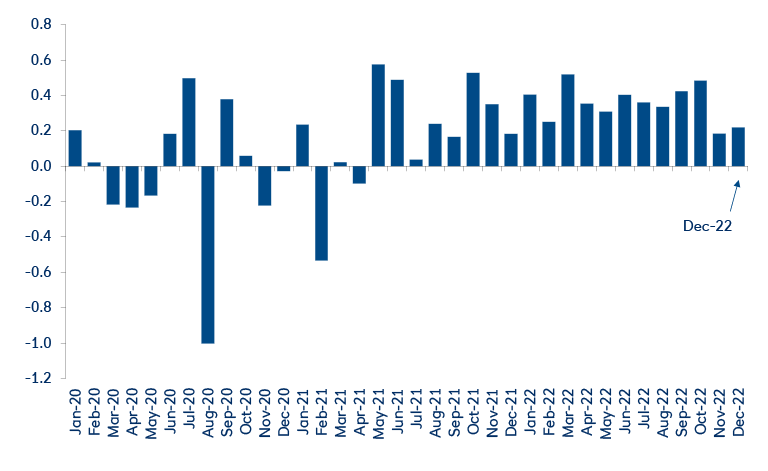

The recent drop in energy prices lends weight to the view that inflation will retreat considerably in 2023. Falling commodity and shipping costs over the last six months coupled with excess inventories suggest that core goods inflation will continue to fall; weaker consumer demand against a backdrop of broader economic sluggishness will also bring down the headline rate.

Core price inflation increases have slowed down

Sources: UK Office for National Statistics (ONS)

UK labour market still strong for now, but it’s cooling

The UK unemployment rate remained unchanged at 3.7% in the three months to November, close to record lows. But as economists are often quick to point out, the labour market is a lagging indicator. While employment rose further in November, forward-looking surveys suggest firms are becoming more cautious, with many scaling back or pausing their hiring plans.

Job vacancies have continued to fall from their peak in the spring, although they’re still above their 2019 average. Redundancies have picked up, but not at a worrying rate.

Meanwhile, workers are receiving their biggest pay rises in years. Average pay growth (excluding bonuses) rose 6.4% year-on-year in November, up from 6.2% in October. The problem for workers is inflation is even higher, meaning pay is still 2.6% lower in real terms.

Separately, labour supply is gradually picking up. High wage growth and inflation represent strong incentives for people not working to return to the labour market. Economic inactivity levels fell by 19,000 in the three months to November, driven by a drop in the number of students, early retirees and long-term sick. Further support is likely to come from rising immigration.

Overall, the heat is beginning to come out of the labour market. But for now, conditions remain relatively tight. Most forecasters only expect a modest rise in the unemployment rate, with a peak of 4.8% by end of the year.

Surveys suggest hiring momentum is waning

Sources: S&P Global, KPMG, REC

The monetary policy tightening cycle seems to be nearing an end

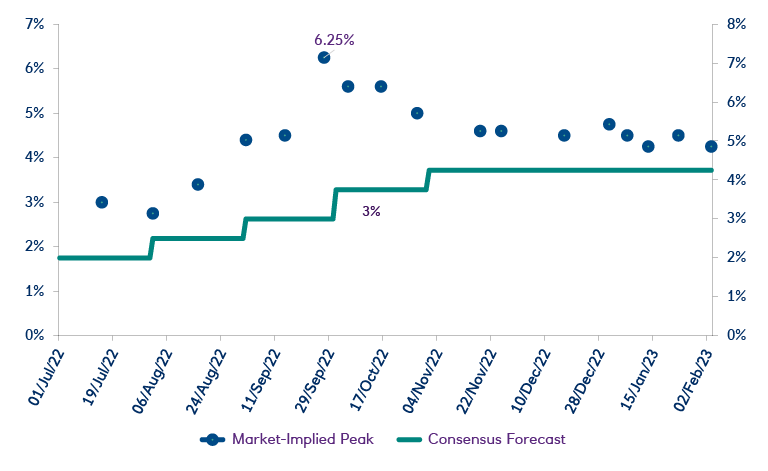

The Bank of England hiked its policy rate by 50 basis points (bp) to 4.0% on 2 February. This is its highest level in 14 years and was the Bank’s 10th consecutive hike. The key question now, though, is when the Bank will call time on tightening. Although another 25bp hike can’t be ruled out in March, there were hints that the end of tightening is near. Its previous guidance on responding “forcefully” to contain inflation was removed, substituted with reference to a “data-dependent” approach. Markets are now pricing in a peak rate closer to 4.25% than the previous 4.50%.

So why might the rate tightening cycle be done? First, inflation is set to fall sharply this year. Second, there’s the lagged impact of all the tightening to date to consider. Higher rates are already dampening economic activity, with a noticeable impact on the housing market: many forecasters are pencilling in a 10% drop in house prices this year.

Given these impacts, why might the Bank of England still have residual concerns about price pressures? The short answer is wage growth and services inflation have been firmer than expected. Recent data underlined that wages are still growing quickly in the private sector, and this could put upwards pressure on inflation.

Is the period of bumper rate rises behind us? Probably. Other central banks are signalling a slowdown in their rate hikes or even an outright halt. The Fed hiked by 25bp at its February meeting, which was the smallest increase since it started tightening in March. The Bank of Canada hiked by 25bp in January but has plans to hold, for now at least. And while the European Central Bank hiked by 50bp last week and signalled another 50bp in March, market pricing suggests it will have finished by the summer. The end is firmly on the horizon, in other words.

Market expectations of the peak bank rate have fallen over the past three months, moving closer to economists’ consensus view

Sources: Bloomberg Finance L.P.

Follow us on social media

Be sure to follow us on LinkedIn to catch all our latest insights as they are published.

Posted in:

Keywords:

Latest insights

How collaboration and innovation can transform AIFs

We surveyed 100 fund influencers and interviewed leaders to explore how tech is reshaping funds and how service providers can support the shift.

03 Nov 2025

Evergreen funds rising popularity

Evergreen funds are experiencing a growth in popularity thanks to their flexibility, liquidity and resilience to market conditions.

24 Mar 2025

Is nature ready to move into the mainstream?

Nature may be a sideline investment strategy for many asset managers but initiatives to protect the natural world are taking root.

16 Jan 2025