The lockdown exit roadmap has been set, cautiously but (hopefully) irreversibly. And come 3 March, the chancellor will table the Budget, outlining the future of the government support schemes which have been so effective in preventing a wider economic fallout. But charting a course out from the extraordinary levels of government spending will be challenging. While markets have awoken to such spending levels, igniting inflation down the road.

Tightrope walking

Government plans to release the country from lockdown are an exercise in acrobatics: balancing greater freedoms with growth in vaccine-induced immunity. Little about England’s lockdown will change this month; the return of schools being a notable exception. But come mid-April, when everyone over 50 has been jabbed, economic life can resume with fanfare. Shops, hairdressers and gyms can reopen; pubs and restaurants can serve outdoors. Indoor service, along with cinemas and hotels will begin mid-May, when second doses will have been administered to all over 70s. And, from late June, the promise of all remaining limits being lifted, paving the way for a strong, sustainable economic recovery. The catch? Nothing is set in stone; all depends on keeping Covid under control.

Slow…

According to the Confederation of British Industry distributive trades survey, the UK’s retail sales balance increased by five points to -45 in February versus January. Trade volumes also contracted at a softer pace. While the improvement is rather unimpressive, it does chime with other forward-looking indicators on retail spending. For instance, retail footfall rose to 38% of its value a year ago for the week ending 20 February, recovering notably from its lows in mid-January. Similarly, the Bank of England’s card-spending data shows an increase of 9% from its January end levels…

But steady

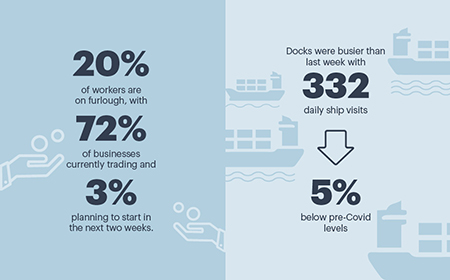

…driven by spending on ‘staples’, with small increases in other categories, as only one in 10 were going out for shopping other than food and medicine. Across all industries, one in five workers are on furlough, with 72% of businesses currently trading and 3% planning to start in the next two weeks. Docks were busier than last week with 332 daily ship visits, 5% below pre-Covid levels. Cases going down, a swift vaccination drive, and increased confidence levels should help these high-frequency indicators to continue to improve in the coming weeks and months.