The oft-mentioned light at the end of the tunnel may just be glowing a little brighter. Falling infection rates coupled with the timely vaccine rollout, the impressive housing market bounceback and an optimistic forecast set by the Bank of England are all stock for the refreshment station of this long marathon. But this is not the only race we are running. A timely reminder last week came on the miles ahead to protect the natural world.

The circus

Admit it. There’s one show in town, and it’s the vaccination programme. The economy bumbles along, with spending about one third lower than last year (32%, based on cards), footfall down two thirds (65%), 18% of the workforce are furloughed and 36% of us worked exclusively from home. And this is probably largely how things will stay until we can ease lockdown. Falling infection rates, while clearly good, don’t sustainably change this. Only vaccination does. So now 12 million of us have had the first dose, running at around half a million doses a day. Every day brings a little more hope.

Getting moving

For several months of last year, it was virtually impossible to move home in the UK, yet such is the scale of the housing market bounceback that 2020 ended up beating 2019 for mortgaged house moves. Over 800,000 mortgages for house purchase were issued. With the stamp duty holiday due to expire in April, the market may need some more policy support to avoid a slowdown. There’s no sign of households’ deposit accumulation slowing down though, with another £20bn increase in December. That brings the rise in liquid savings in 2020 to around £130bn, according to the Bank of England, and 2021’s economic prospects hang on whether people are willing and able to spend it.

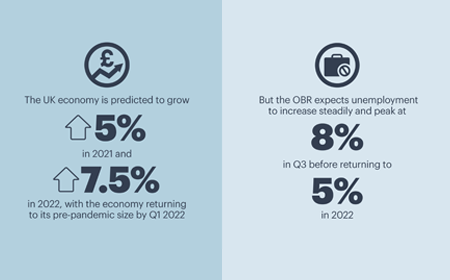

Stand ready

The BoE’s latest policy meeting could be described as all talk, no action. No change in bank rate (0.1%) or asset purchases (QE). But banks must be operationally ready to implement negative rates in six months’ time. That doesn’t mean they will be used, just available in the policy toolbox. If the BoE’s racy forecasts prove correct, the next interest rate move will be up, not down. A rapid economic recovery is expected from Q2 as the vaccine rollout enables lockdown restrictions to be lifted. Economic growth of 5% this year and 7.25% in 2022 should see the UK economy return to its pre-pandemic size by Q1 2022. Meanwhile, unemployment is set to peak just shy of 8% in Q3 before returning to 5% in 2022.