01 Feb 2024

Navigating change and what lies ahead for fund finance

Even if interest rate cuts are just around the corner, it’s unclear how quickly they’ll fall or at what level they’ll eventually settle.

At the end of last year, the market was starting to feel optimistic about the prospect of swift interest rate cuts as inflation continued to decline. While the unexpected spike in pace of price rises in December complicated the outlook, optimism for eventual rate reductions remains.

As welcome as the reduction would be, it should be viewed in the context of what came before. After nearly a decade of structurally low interest rates, skyrocketing inflation prompted the Bank of England to raise its base rate from just 0.1% in December 2021 to its current level of 5.25%. Inflation peaked at 11% in October 2022, and though it has fallen to 4% by December 2023, the outlook is further complicated by geopolitical conflict and trade disruption. Even if interest rate cuts are just around the corner, it’s unclear how quickly they’ll fall – or even whether they’ll eventually settle at levels seen just before the covid-19 pandemic.

A return to the old days or a new normal?

“I guess it’s a question of whether this is the new normal”, says James Hamelin, a director at RBS International, who specialises in fund finance. “Is what we’ve seen, which has significantly impacted fundraising, just a passing blip or does it signify a more enduring shift for the industry?”

Soaring interest rates in Europe and the US have impacted activity levels in private markets, with increased financing costs and concerns about macroeconomic conditions and geopolitical events contributing to a slowdown in deal-making. This, in turn, has meant distributions to investors have collapsed.

In addition, public market values have declined by more than their private market counterparts, resulting in the "denominator effect" where investors find themselves over-exposed to private markets.

“When trouble hits, you tend to see public valuations drop faster and further than private valuations,” says Danny Peel, partner, and head of finance at Travers Smith. “So, over a short period of time, an investor might look at its portfolio and find that it's gone from (say) having 10% of its portfolio allocated to the private markets to 20% or even 25% – purely because of fluctuations in the underlying valuations.”

For many investors, the shifting balance in their portfolio means either an inability to make further investments in the private markets or significant restrictions, leading to a tightening of capital. And the effect of this can be exacerbated by the fact that it is typically the larger, institutional investors that are most impacted.

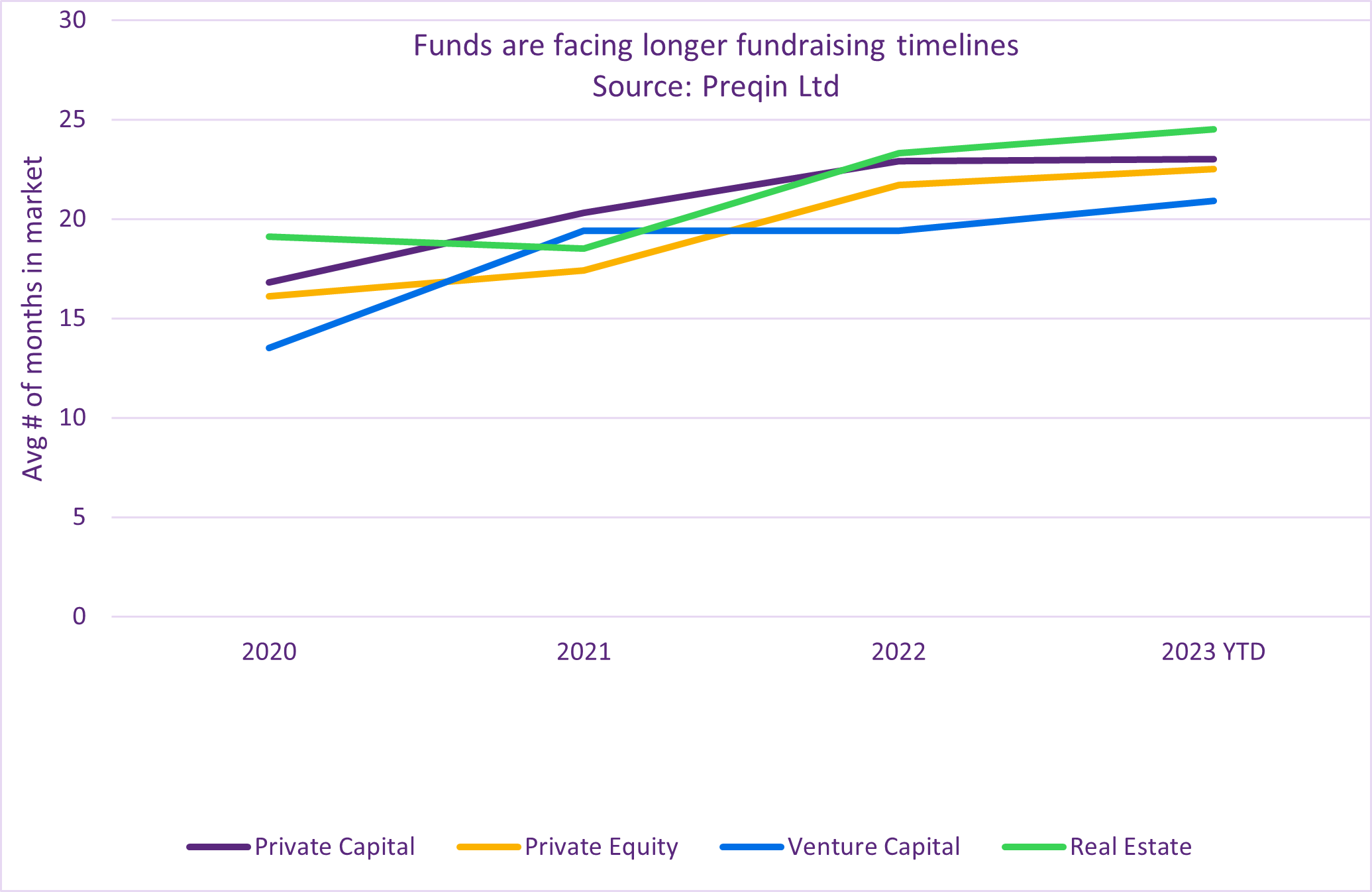

According to data provided by Preqin1, the average number of months in the market for private capital has lengthened significantly since 2020, with private capital increasing from 16.8 months in 2020 to 23 months in 2023. Taking a sector view, private equity has risen from 16.1 months to 22.5 months, private debt 19.7 months to 25.3 months, venture capital from 13.5 to 20.9 months and real estate from 19.1 months to 24.5 months.

This cocktail of challenges has resulted in by far the most difficult fundraising market in recent times.

“We’ve certainly found in the last 12 months that fund finance deals have just been moving out and out,” says James. “So, a first close that was supposed to happen in Q1 last year, potentially still hasn’t happened, and might now be looking at the first quarter of this year, so there’s been a real shift in timings.”

One other challenge highlighted by James on the fund finance side is a concentrated investor base early in the fundraising cycle. “A lot of managers have become accustomed to putting in place a subscription line at first close. But with the trend of smaller and more concentrated investor closes, this process is increasingly challenging. Managers may find themselves in a position where they need to wait until a sufficient number of institutional investors have closed their commitments before lenders are willing to take on the associated risks.”

Diversifying the investor base

While in the long term, the fundraising market will still need a return of new institutional capital, the sector has been able to mitigate part of the impact by diversifying its investor base and attracting greater amounts of capital from high-net-worth individuals (HNWs) and family offices.

“There’s a lot of institutional investors that will be well allocated in this space, and potentially holding back any further investments for now,” explains James, “but there’s a lot of private wealth out there that is growing in various regions, so we are seeing more and more family office and HNW money come into the investor bases.”

However, this diversification poses challenges related to credit quality assessment. Family offices often lack publicly available information, requiring in-depth conversations between lenders and asset manager clients to assess their creditworthiness. As a result, the amount that a fund might be able to borrow against their investor base through a subscription facility is potentially reduced due to the higher risk associated with it.

Though it is still in its early stages, the mechanism by which the capital available from HNWs can be invested into the private markets is showing signs of maturing and has support from a wide variety of stakeholders. Policymakers hope it will help to fuel growth; investors want the exposure to the sorts of returns that the private markets (and alternative asset managers in particular) have been able to generate; and the asset managers themselves see a substantial pool of untapped capital.

Retail investment can be structured in a variety of ways, but one route is via the development of specific retail funds that group the investors together, which in addition to increasing the amount of capital, also spreads the risk.

As Danny explains: “One of the investment banks might say, ‘We've got 500 of our HNW investors together, and each of them have committed $1 million to an investment vehicle we've established, and we want to use this vehicle to invest in your fund. So that's a $500 million commitment that's coming in from HNW investors, and the asset manager – as well as any fund finance provider – can take comfort in the knowledge that they’ve been vetted by a major investment bank.”

“As that market becomes more sophisticated, and there's an ever-increasing number of people who are looking at private assets on the retail side of the sector, such as in private equity for example, then I think that will create opportunities. But it's going to have to be on a more diversified basis.”

Cautious cause for optimism

Looking ahead, forecasting precise outcomes is challenging, however there is a sense of cautious optimism prevailing.

“I think what we're hearing from the market is that things are starting to stabilise, and there is definitely optimism,” says James.

Similarly, Danny also expects there to be an easing in general fundraising conditions in the latter part of this year. However, given the length of time that investors have been sat on their hands, it might take time to fully come through.

Evidence of this growing backlog and increased competition for funds in the market can be found in the fact that the number of funds seeking capital has more than doubled from 5,244 in January 2020 to 12,282 in January 2023, according to data provided by Preqin2. “Fundraising is a cycle, with different asset managers out raising capital at different times. However, when managers are having to extend their fundraising periods, the market can get very crowded", Danny says.

Asset managers that need to go out and raise capital therefore face the choice of attempting to raise money when many of their peers are also out there or holding back and waiting for the market to normalise again. They might be able to hold back if they still have capital to spend, but if not, they face some difficult choices: do they go out regardless, change strategy, move to a deal-by-deal approach, or do something else?

The new normal for fund finance may be far from clear. But, with interest rates hopefully starting to fall this year, fundraising conditions improving, and deal volumes rising, the asset management community should begin to feel a collective sense of relief.

If you want to discuss how to navigate the current market and the impact on your organisation, please contact your relationship director.

Source 1&2: Preqin Ltd

Posted in:

Keywords:

Latest insights

How collaboration and innovation can transform AIFs

We surveyed 100 fund influencers and interviewed leaders to explore how tech is reshaping funds and how service providers can support the shift.

03 Nov 2025

Evergreen funds rising popularity

Evergreen funds are experiencing a growth in popularity thanks to their flexibility, liquidity and resilience to market conditions.

24 Mar 2025

Is nature ready to move into the mainstream?

Nature may be a sideline investment strategy for many asset managers but initiatives to protect the natural world are taking root.

16 Jan 2025